It has been a brutally volatile week across global markets, driven by a whirlwind of US tariff implementations, abrupt reversals, and rapid retaliatons. Investors were left scrambling to make sense of the White House’s constantly shifting trade stance. We won’t attempt to recap every step of the tariff saga, when even members of the administration seemed unable to track the unfolding policy moves.

The most consequential outcome of the week was the broad-based pressure on US assets. The sharp selloff in Treasuries drew the most concern, raising alarms over whether the bedrock of the financial markets is beginning to erode. That said, while the jump in yields was certainly eye-catching, it has yet to cross the threshold into full-blown crisis territory.

US stocks, after plunging to their lowest levels in months mid-week, managed to stage a strong rebound. Key technical support levels held, keeping the long-term uptrend intact—for now. However, that doesn’t mean the risks are gone. If the mounting tariffs ultimately tip the US into recession, the bounce may prove to be nothing more than a bear market rally.

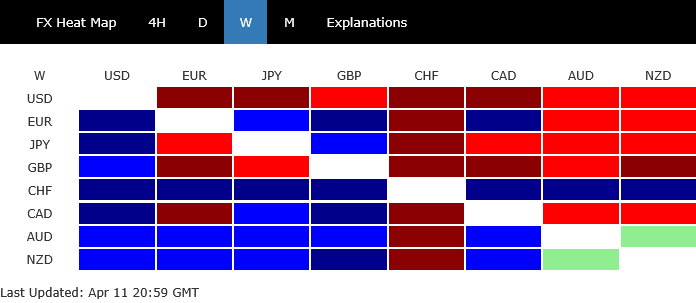

Dollar also struggled, ending as the week’s worst performer. Despite rising yields and some risk-off mood, neither provided the greenback any meaningful support. Dollar Index is now on the verge of resuming its broader medium-term downtrend.

In the broader forex markets, Sterling and Yen also underperformed. On the other end, Swiss Franc stood tall as the market’s safe-haven anchor, followed by Australian and New Zealand Dollars. Euro and Canadian Dollar ended the week in middle ground.

{kind=link}

Tariff Shock and Yield Spike Rattle Markets; Not a Crisis Yet, But Warnings Are Flashing

The essence of the market chaos: US reciprocal tariffs officially went into effect—only to be paused within hours to allow room for negotiation, except for China. On the surface, that might have calmed markets. And indeed, it opened the door to dialogue, with Taiwan reportedly holding the first video talks, while delegations from the EU and Japan are en route for face-to-face meetings in Washington in the coming days.

But on the other side of the equation was deepening hostilities between the US and China. Both sides escalated tariffs beyond economically meaningful levels, effectively moving toward full-scale trade decoupling. The narrative is no longer about negotiation—it’s about economic separation.

What spooked markets the most wasn’t just the trade conflict, but the simultaneous selloff in US assets—equities, Dollar, and perhaps most importantly, Treasuries. This rare alignment of outflows suggested something deeper: a loss of confidence. Some speculate this is precisely why US President Donald Trump reversed course and paused the reciprocal tariffs—because of the violent reaction in the bond market.

Indeed, Trump and his economic advisors have repeatedly cited the importance of keeping bond yields low to support the broader economic agenda. As yields spiked and refinancing costs soared, concerns within the White House likely escalated. A persistent rise in yields would undermine everything from fiscal stimulus to housing affordability and corporate balance sheets.

There are several theories about what triggered the Treasury selloff. Some point to the unwinding of the “Treasury basis trade”—a leveraged strategy used by hedge funds that collapsed under margin stress. Others blame foreign governments, particularly China, for dumping US debt in retaliation.

But perhaps the most straightforward explanation is the simplest: long-term investors are losing interest in US assets, shifting instead into alternatives like Gold in this time of uncertainty, which surged to fresh record highs this week.

Importantly, not all global bond markets are suffering. Germany’s 10-year yield remained within a calm 2.5–2.7% range.

{kind=link}

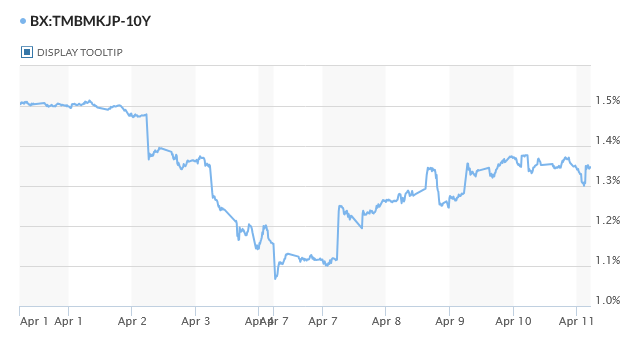

Japan’s 10-year yield held steady around 1.3–1.4% after being pulled up by US yields.

{kind=link}

In contrast, US 10-year yields soared, nearing 4.6%, a stark rise from just 3.89% a week ago.

Technically, the picture in US 10-year yields is worrying but not yet in panic mode. For the near term, the decline from 4.809 should have bottomed at 3.886% as a correction. As long as 4.289 support holds, further rise toward 4.809 is expected.

{kind=link}

That said, this is still within the bounds of a broad consolidation pattern from the 2023 peak at 4.997%. Current rally might just be one of the legs.

{kind=link}

However, if 10-year Treasury yields were to break decisively above the symbolic 5% level, the impact could be seismic. Borrowing costs across the economy would surge along, from mortgages to corporate debt, tightening financial conditions at a pace that could choke off growth.

Beyond the US, such a move could trigger…

Read More: A Whirlwind Week Leaves US Assets Reeling Amid Tariff Turmoil