Forex markets remained subdued today, with muted reactions to key economic data. Dollar held broadly higher as traders focused on the US-Russia peace talks, where both sides agreed to continue discussions on ending Russia’s invasion of Ukraine. However, meaningful progress is unlikely without direct involvement from Ukraine and European nations, keeping market uncertainty elevated.

Canadian Dollar traded mixed following slightly stronger-than-expected core inflation data. Despite this, with headline CPI below 2% and CPI common just above 2%, BoC is still expected to gradually lower rates toward neutral levels.

British Pound showed little reaction to strong UK labor market data, including strong wage growth. BoE Governor Andrew Bailey commented that the figures did not alter the central bank’s outlook, keeping rate expectations steady. Similarly, Euro ignored a notable improvement in German economic sentiment, which suggests the economy may finally be stabilizing.

Australian Dollar remains supported following RBA’s cautious rate cut, with the central bank signaling that the easing cycle will proceed gradually and may not be as deep as previously expected.

Looking ahead, RBNZ rate decision is the primary focus in the upcoming Asian session, where markets anticipate a 50bps rate cut, bringing the OCR down to 3.75%, moving closer to neutral levels. A key point of interest will be whether RBNZ signals a slowdown in the pace of easing, and traders will analyze economic projections for insights into the terminal rate.

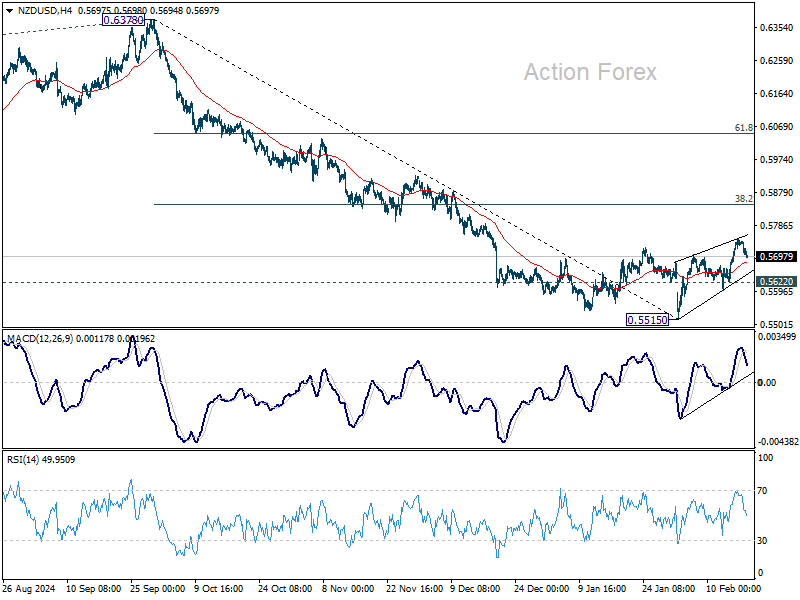

Technically, NZD/USD’s rebound from 0.5515 is seen as a correction to the fall from 0.6378. While another rise cannot be ruled out, upside should be limited by 38.2% retracement of 0.6378 to 0.5515 at 0.5848. Break of 0.5622 minors support will argue that the corrective bounce has completed, and bring retest of 0.5515 low.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.24%. CAC is up 0.31%. UK 10-year yield is up 0.032 at 4.570. Germany 10-year yield is up 0.012 at 2.504. Earlier in Asia, Nikkei rose 0.25%. Hong Kong HSI rose 1.59%. China Shanghai SSE fell -0.93%. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield rose 0.0435 to 1.436.

Canada’s CPI rises to 1.9% in Jan, core inflation ticks up

Canada’s headline CPI increased from 1.8% yoy to 1.9% yoy in January, in line with expectations. The rise was driven by higher energy costs, particularly gasoline and natural gas, while GST/HST tax break introduced in December helped offset broader price pressures.

Food prices fell -0.6% yoy, marking the first annual decline since May 2017, led by a record -5.1% yoy drop in restaurant food prices.

On a monthly basis, CPI rose 0.1% mom, rebounding from December’s -0.4% mom decline.

Core inflation strengthened, with CPI median rising to 2.7% yoy from 2.6% yoy, CPI trimmed increasing to 2.7% yoy from 2.5% yoy, and CPI common edging up to 2.2% yoy from 2.0% yoy.

German ZEW jumps to 26 in Feb, optimism ahead of elections

German ZEW Economic Sentiment Index surged from 10.3 to 26.0 in February, surpassing expectations of 20.2 and reflecting growing optimism about Germany’s economic outlook. Current Situation Index also showed a slight improvement, rising from -90.4 to -88.5, beating forecasts of -89.0.

Eurozone ZEW Economic Sentiment rose from 18.0 to 24.2, falling short of the anticipated 25.4, while the Current Situation Index climbed by 8.5 points to -45.3.

According to ZEW President Achim Wambach, the sharp rise in expectations is likely driven by hopes for a “new German government capable of action” ahead of the federal election, alongside expectations for a rebound in private consumption over the next six months.

UK wages growth accelerates in Dec, payrolled employment rose 21k in Jan

The latest UK labor market data presents a mixed picture, with payrolled employment rising by 21k (0.1% mom) in January, but the Claimant Count increasing by 22 to 1.75 million. Meanwhile, median monthly pay reached £2,467, reflecting a 5.7% yoy increase, reinforcing concerns about wage-driven inflation pressures.

Looking at the broader employment trend, data for the three months to December showed that the employment rate edged up by 0.1 percentage point to 74.9%, while the unemployment rate also ticked higher by 0.1 percentage point to 4.4%.

Wage pressures remain elevated, with average earnings including bonuses accelerating from 5.5% yoy to 6.0% yoy, and earnings excluding bonuses rising from 5.6% yoy to 5.9% yoy.

RBA cuts rates, but warns against easing too much too soon

RBA lowered its cash rate target by 25bps to 4.10%, as widely anticipated, but signaled a cautious approach to further easing.

In its statement, the central bank emphasized that monetary policy will remain…

Read More: Muted Forex Action as Traders Overlook Data, Await RBNZ Cut